Click to download the PDF

Stocks Hit New Highs as the Pandemic Recedes

Last quarter, we discussed the strong start to 2021 as the market experienced solid gains. The second quarter continued that trend, with the S&P 500 rising to another record high.

Throughout the quarter, COVID-19 cases substantially declined in the U.S. This, combined with a near-total economic reopening across the country, led a surge in economic growth that helped stocks rally to new highs over the past three months.

A number of positive developments led the S&P 500 to its strong start in the second quarter. The pace of vaccinations in the U.S. accelerated meaningfully in April, with daily vaccinations hitting a peak of more than three million per day by the middle of the month. The number of new COVID-19 infections fell from approximately 77,000 daily new cases at the beginning of April to less than 60,000 daily new cases during the last week of the month. Numerous states began to fully reopen their economies or announced plans to do so in the near future. That served as a positive signal to investors that a return to a pre- pandemic normal was now likely just a matter of time.

The Federal Reserve reiterated its support for the economy and promised not to remove any accommodation in the near term. That continued “safety net” gave investors confidence in the future economic outlook and the sustainability of the economic recovery. Finally, first-quarter corporate earnings were very strong, as the vast majority of U.S. companies beat earnings estimates. These positive factors helped stocks rally throughout the month, as the S&P 500 hit a new record above 4,200 during the final days of April.

The rally paused in May thanks to uncertainty regarding inflation, the labor market and when the Federal Reserve would begin to reduce, or taper, its quantitative easing (QE) program. A disappointing jobs number in early May implied the labor market might not be recovering as quickly as expected. That, combined with inflation metrics hitting multi-decade highs, elicited some concern the economic recovery might not be as strong as forecasted, and that a return of inflation might make the Federal Reserve begin to reduce accommodation earlier than previously expected.

After some volatility early in the month, it became apparent that the lackluster job growth was more a function of a labor supply issue rather than there not being enough jobs available. Investors came to believe that issue will resolve itself as the economy and society continues to return to a pre- pandemic normal.

Federal Reserve officials reiterated their long-held position that any increase in inflation would be temporary and due to pandemic-related supply chain disruptions. They do not expect a return of the inflation problems of the 1970’s. Investors were comforted enough for stocks to rebound in mid-May and the month closed with a small gain.

Stocks resumed the rally in early June, as more state economies opened (most notably California). Measures of economic activity remained strong, and certain inflation statistics implied that inflation pressures were starting to ease, possibly validating the Federal Reserve’s belief that surging inflation is just temporary.

The June Federal Reserve meeting provided a small surprise to markets, as it revealed that Federal Reserve officials began discussions about when to reduce the current quantitative easing program. Federal Reserve forecasts showed interest rates could start to rise late in 2022, sooner than previously expected. Those two surprises caused some mild market volatility late in June, although ultimately investors remained confident that the Federal Reserve will not remove economic support too quickly. The S&P 500 went on to hit another record high during the last few days of the quarter.

In sum, the strong gains of the second quarter and the first half of 2021 reflected continued government support for the economy combined with a material improvement in the pandemic in the U.S. As we start the second half of 2021, we are happy to say the world looks a lot more like it did pre-pandemic than it did for most of 2020, and that sentiment is supportive of risk assets going forward.

2nd Quarter Performance Review

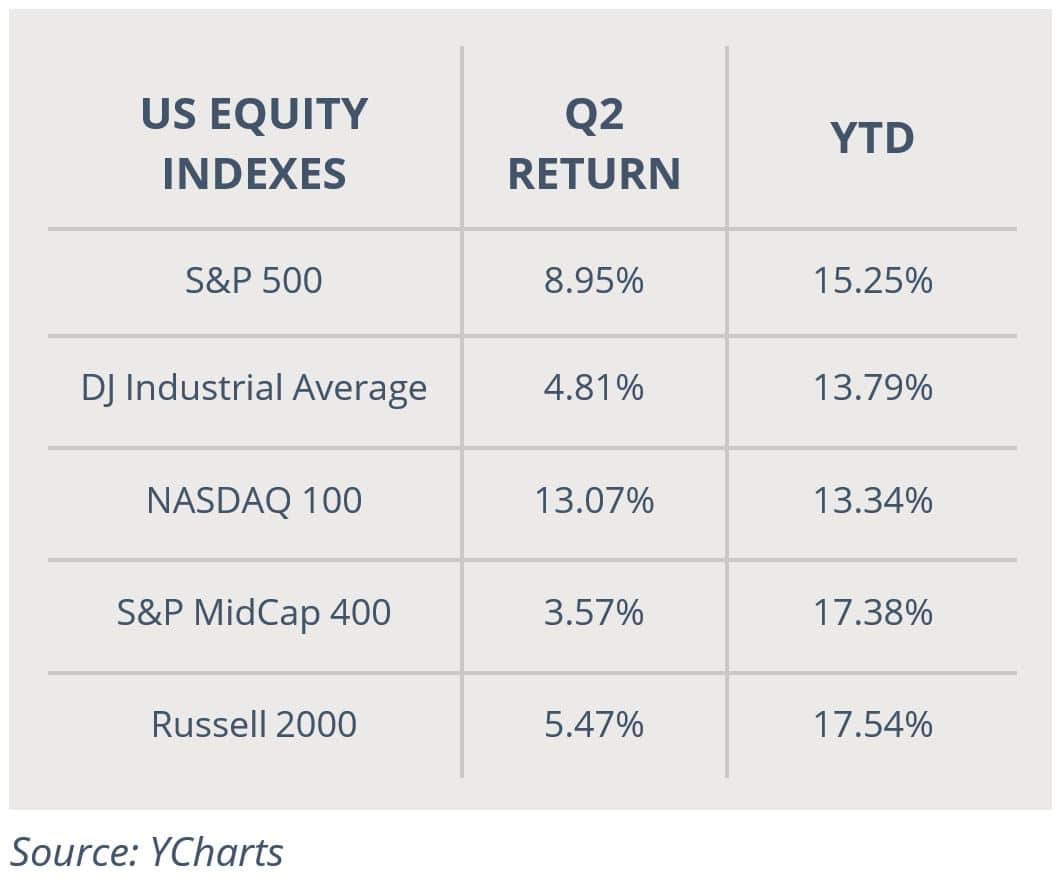

In a reversal from the first quarter, the Nasdaq outperformed both the S&P 500 and Dow Jones Industrial Average thanks to a June rally in technology shares. Investors began to consider that the intensity of the economic recovery had possibly peaked now that virtually all state economies had fully reopened. Additionally, the Federal Reserve signaling that it has begun discussions to reduce its QE program made some investors nervous that economic growth could slow in the future. This contributed to the rotation back towards technology stocks, which tend to be less sensitive to changes in economic growth compared to other market sectors.

By market capitalization, large-cap stocks outperformed small-cap stocks, which was a reversal from the previous two quarters. Small- cap stocks tend to outperform during periods of accelerating economic growth, like we saw in the fourth quarter of 2020 and the first quarter of 2021. But with investors considering that the intensity of the economic recovery may have peaked in the second quarter and that the Federal Reserve may reduce QE in the future, they rotated back into large caps as the outlook for future economic growth became slightly less certain.

From an investment-style standpoint, growth handily outperformed value thanks to the tech sector rally. Investors positioned for the possibility that the intensity of the economic recovery may wane in the coming months.

On a sector level, 10 of the 11 S&P 500 sectors realized positive returns in the second quarter with real estate and tech outperforming. The real estate sector was boosted by a decline in mortgage rates combined with consumers returning to malls and shopping centers. A drop in Treasury bond yields helped fuel the rotation back to tech stocks.

Sector laggards last quarter included consumer staples and utilities as the former registered a small gain while the latter was the only S&P 500 sector to finish negative for the quarter. Those traditionally defensive sectors outperform when investors expect an outright economic slowdown. While some investors believe the acceleration in the economic recovery may have peaked, most analysts are expecting the economic recovery to continue, just at a moderating pace, making defensive sectors such as utilities and consumer staples less attractive.

Internationally, foreign markets saw positive returns in the second quarter thanks to further declines in COVID-19 cases, rising vaccination rates, and more widespread economic re-openings across the EU and UK.

Emerging markets also rallied in the second quarter on hopes of a global economic recovery. They slightly underperformed foreign developed markets as the Chinese government reduced support for its economy following a large increase in inflation indicators. Foreign developed markets again lagged the S&P 500.

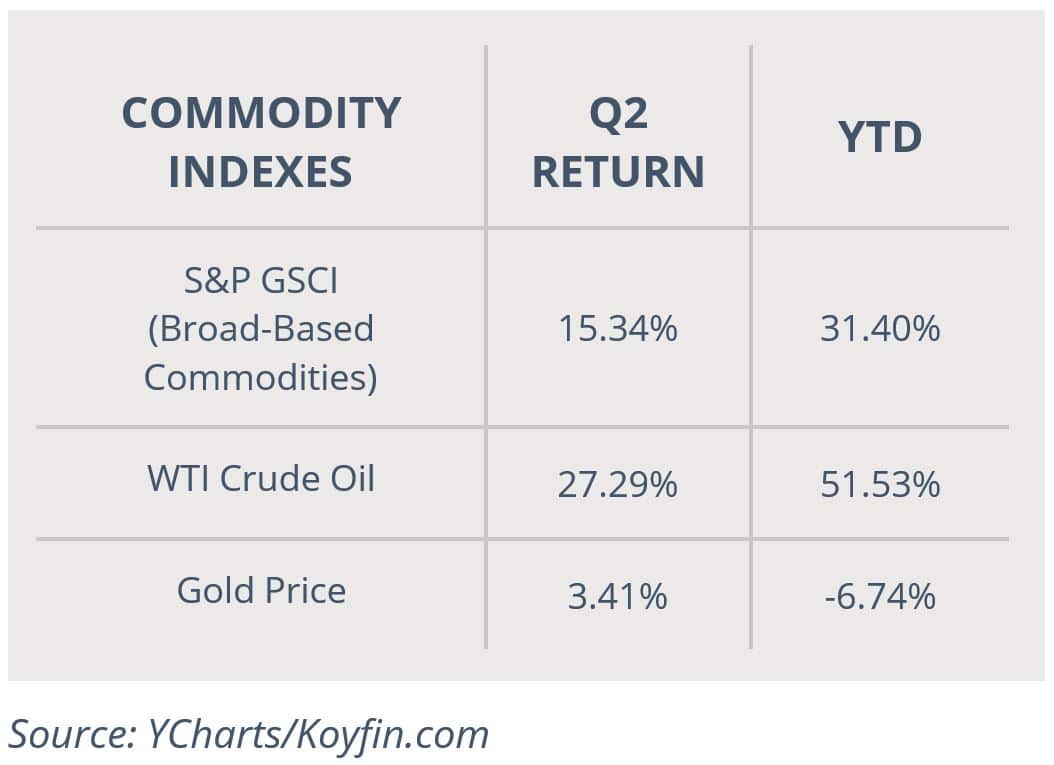

Commodities posted strong gains for the third quarter in a row, and once again, outperformed the S&P 500 over the past three months. Major commodity indices were led higher by another large rally in crude oil futures as demand rose for both oil and refined products following the U.S. and European economic re-openings. Despite the resumption of nuclear negotiations between the U.S. and Iran, sanctions remained in place preventing Iran from selling oil on the global market. Compliance to self-imposed production targets by members of “OPEC+” remained historically high, keeping global oil supplies subdued.

Gold posted a small gain as investors rotated back to it following a spike in inflation metrics. Combined with an increase in volatility in Bitcoin, this sent money back into more traditional non-correlated, safe-haven assets.

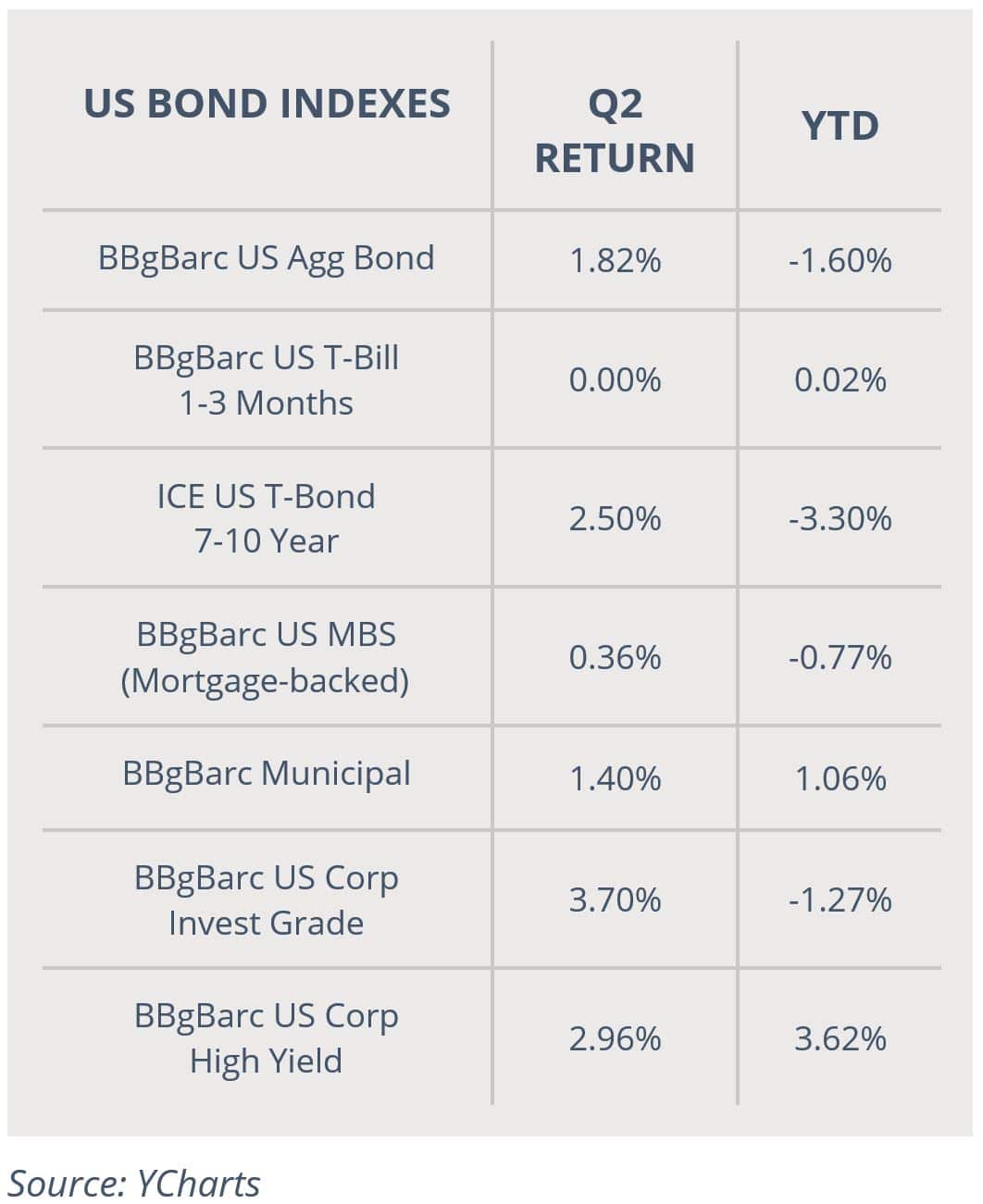

Switching to fixed income markets, second quarter total returns for most bond classes were positive, a reversal from the first quarter. Despite inflation indicators surging to multi-year highs in recent months, investors viewed those increases as temporary phenomena related to the global economic reopening and short-term supply chain issues. Investors took advantage of relatively higher bond yields in the second quarter.

Looking deeper into the bond markets, longer-duration bonds outperformed those with shorter durations in the first quarter. That substantial outperformance was driven by the market’s view that the increase in inflation was indeed temporary, combined with effective messaging by the Federal Reserve that interest rates would remain near 0% for the foreseeable future.

In the corporate debt markets, investment grade bonds solidly outperformed lower-quality, higher-yielding bonds. That investment grade outperformance reflects confidence in the sustainability of the U.S. economic recovery but also acknowledges that the pace of economic growth may moderate in the coming months.

3rd Quarter Market Outlook

Markets reflected a legitimate improvement in the macroeconomic outlook during the second quarter as substantial progress against the pandemic helped underwrite the gains in stocks over the past three months. But that strong performance should not be taken as a signal that risks no longer remain. The next three months will bring important clarity on several unknowns including inflation, future Federal Reserve policy, and the pandemic.

Regarding inflation, some metrics in June implied that the spike in inflation during the second quarter is starting to reverse, but that debate is far from settled. No one knows what the trillions in pandemic stimulus combined with 0% interest rates and the Federal Reserve’s ongoing QE program will do to inflation over the longer term. If this sudden surge in inflation is temporary, we should see more conclusive evidence of that during the third quarter.

The Federal Reserve, meanwhile, has started the process of communicating how it will begin to reduce support for the economy via “tapering,” or reducing, its quantitative easing program. The last time the Federal Reserve had to deliver that message, they triggered the “Taper Tantrum” of 2013, which saw stock and bond market volatility rise significantly. It remains to be seen how expected removal of accommodation and an eventual increase in interest rates will impact markets.

Finally, despite significant progress against COVID-19 here in the U.S., the pandemic is not over. Vaccination rates for most countries are well behind that of the United States. The second quarter saw an explosion of COVID-19 cases in India, and an outbreak in China. England delayed its planned economic reopening over concerns about the spread of the “Delta” COVID-19 variant that was behind the surge in cases in India. Then, both Australia and South Africa reimplemented local lockdowns due to rising cases of the Delta variant. Point being, there remains a possibility that a new COVID-19 variant appears and renders the vaccines less effective. If that happens, markets will become concerned that progress towards a return to economic normal will be reversed, and that will cause volatility.

There has been material progress made in the United States against the pandemic, and life as we know it has thankfully returned mostly to normal. Yet now is not a time to become complacent as numerous economic and pandemic-related risks remain. The macroeconomic outlook is still decidedly positive. We should all remain prepared, however, for bouts of market volatility.

Risks remain to the markets and the economy, as they always do. It is important to remember that a well-executed and diversified, long-term- focused financial plan can overcome bouts of even intense volatility, like we have seen over the last 18 months.

At Krilogy®, we understand the risks facing both the markets and the economy, and we are committed to helping you effectively navigate this still-challenging investment environment.

Successful investing is a marathon, not a sprint. Even temporary bouts of volatility like we experienced during the height of the pandemic are unlikely to alter a diversified approach set up to meet your long-term investment goals.

It is critical for you to stay invested, remain patient, and stick to your plan, which has been developed to establish a unique, personal allocation target based on your financial position, risk tolerance, and investment timeline.

The economic and medical progress achieved so far in 2021 notwithstanding, we remain vigilant towards risks to portfolios and the economy. We thank you for your ongoing confidence and trust. Please rest assured that the entire Krilogy® team remains dedicated to helping you successfully navigate this market environment.

Important Disclosures

Information contained in this document is provided by an independent third party, Ned Davis Research. While believed to be accurate, Krilogy® has not independently confirmed each piece of information.

Investment Advisory Services offered through Krilogy®, an SEC Registered Investment Advisor.

Please review Krilogy’s Form ADV 2A carefully prior to investing. All expressions of opinion are subject to change. This information is distributed for educational purposes only. It should not be construed as individualized advice or recommendations suitable for the reader.

Diversification does not eliminate the risk of market loss. Investments involve risk and unless otherwise stated, are not guaranteed. Investors should understand the risks involved of owning investments, including interest rate risk, credit risk and market risk. Investment risks include loss of principal and fluctuating value. There is no guarantee an investing strategy will be successful. Past performance is not a guarantee of future results.